One of the more challenging aspects of underwriting commercial real estate investments is that returns can be measured in several different ways. Each metric offers a slightly different lens, with its own strengths and shortcomings. As a result, experienced investors rarely rely on a single metric in isolation, instead reviewing a combination of measures to understand both risk and return.

In this article, we examine one of the most commonly used metrics—the Equity Multiple in commercial real estate. We explain what it is, how to calculate the equity multiple, its advantages and drawbacks, and what investors typically consider to be a “good” result. By the end, investors should be able to incorporate the Equity Multiple into their broader pre-investment due diligence process.

What is the Equity Multiple?

The Equity Multiple is a commercial real estate performance metric that measures an investment’s potential profitability as a function of the original equity invested. The result is expressed as a number—such as 1.8x or 2.1x—representing how many times an investor’s initial capital is returned over the life of the investment.

How is the Equity Multiple Calculated?

The equity multiple formula is straightforward:

Equity Multiple = Total Cash Received / Total Equity Invested

While the formula itself is simple, determining the correct inputs requires careful underwriting.

Equity Multiple Calculation Example

Consider a property purchased for $1,000,000 with $750,000 in debt, resulting in a $250,000 equity investment. Assume the property generates $75,000 in annual cash flow for five years and produces a $150,000 gain upon sale.

- Total cash flow: $75,000 × 5 = $375,000

- Sale proceeds: $150,000

- Total money received: $525,000

The equity multiple is therefore:

$525,000 ÷ $250,000 = 2.10x

In this scenario, investors would expect to receive just over twice their original equity investment over the holding period.

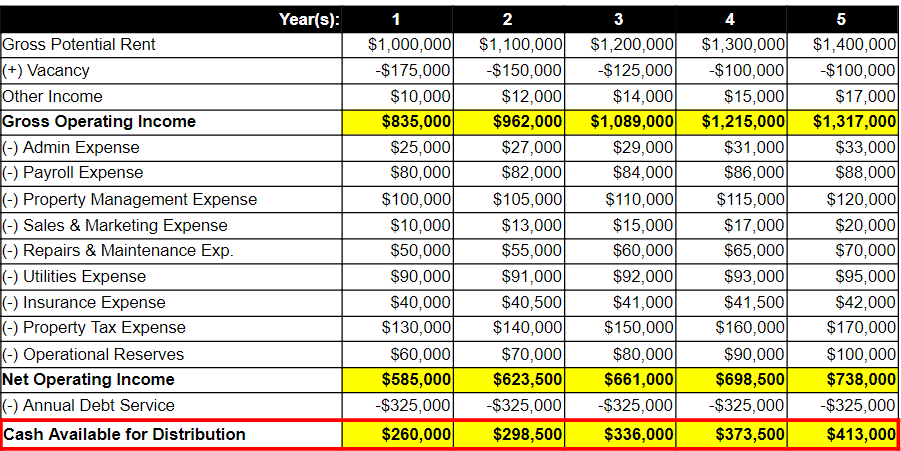

What is a Proforma?

Before calculating return metrics, investors typically create a proforma, which is a forward-looking financial projection of a property’s operating performance. A proforma estimates income and expenses over a planned holding period—often five to ten years. Using past performance and market dynamics as a guide, income and expenses are projected for a planned holding period, usually 5-10 years, and the end result could look something like the following table:

The most important line in the proforma for return analysis is Cash Available for Distribution. This figure represents the cash remaining after operating expenses and debt service and forms the basis for estimating total cash received by investors.

Components of the Equity Multiple Formula

Total Money Received

Total money received represents the cumulative cash returned to investors over the planned holding period. This includes periodic cash distributions as well as net proceeds from the sale of the property.

Because this figure is based on projections, it is inherently an estimate. Conservative assumptions around income growth, expenses, and exit pricing are critical to avoid overstating potential returns. Sound proforma construction is one of the most important elements of disciplined pre-investment due diligence.

Total Money Invested

Total money invested refers to the equity capital contributed by investors.

- In an all-cash acquisition, this amount equals the purchase price.

- More commonly, properties are acquired using a combination of debt and equity. In these cases, total equity invested equals the purchase price minus the loan amount (including any preferred equity, if applicable).

What is a “Good” Equity Multiple?

What constitutes a “good” equity multiple depends on an investor’s return objectives and risk tolerance. Higher equity multiples generally require accepting higher risk, while lower-risk investments often produce more modest multiples.

That said, an equity multiple of 2.00x or greater is commonly viewed as attractive in many commercial real estate contexts, particularly when achieved over a reasonable time horizon.

Why Use the Equity Multiple?

The primary advantage of the Equity Multiple is its simplicity. It is easy to calculate, easy to interpret, and clearly shows an investor’s absolute return relative to their initial capital.

The primary limitation is that it does not account for time. Earning a 2.00x equity multiple over three years is materially different from earning the same multiple over ten years. As a result, the Equity Multiple alone can be misleading if used without additional context.

What is the Internal Rate of Return?

The Internal Rate of Return (IRR) measures the annualized return on invested capital while accounting for the timing of cash flows. It reflects the time value of money—the principle that a dollar received today is worth more than a dollar received in the future.

IRR uses the same cash flow inputs as the Equity Multiple but incorporates timing, making it more complex to calculate. Most investors rely on spreadsheet software to compute IRR and often target returns in the mid-single-digit to low-double-digit range, depending on asset type and risk profile.

While IRR accounts for time, it does not indicate total profit and can be skewed by large early-period cash flows.

IRR and Equity Multiple Together

Used independently, both metrics can be misleading. IRR is most useful when comparing investments with similar holding periods, while the Equity Multiple is better at illustrating absolute return.

Together, they provide a more balanced assessment—capturing both how much investors may earn and how long it may take to earn it.

Equity Multiple and Real Estate Syndications

Evaluating commercial real estate opportunities requires experience, judgment, and repetition. Building accurate proformas, stress-testing assumptions, and interpreting return metrics across different asset classes can be challenging for individual investors.

Private equity real estate firms often address this complexity through syndications, where the firm sources, underwrites, finances, and manages properties on behalf of passive investors. For those without the time or desire to perform detailed underwriting independently, this structure can provide access to institutional-quality analysis and execution.

Summary of the Equity Multiple

The Equity Multiple is a foundational return metric in commercial real estate investing, expressing total cash received as a multiple of equity invested.

Its simplicity makes it useful, but its lack of time sensitivity limits its standalone value. When evaluated alongside IRR, the Equity Multiple helps investors better understand both absolute returns and the efficiency with which those returns are generated.