On March 11th, 2020 the World Health Organization declared the disease caused by the novel coronavirus, COVID 19, to be a global pandemic. Two days later, on March 13th, the United States Centers for Disease Control (CDC) declared the COVID 19 outbreak in the United States to be a national emergency.

In the days and weeks that followed, private businesses and government authorities scrambled to take steps to contain the outbreak. Because the virus is transmitted through airborne droplets, the most extreme of these measures shuttered popular gathering spots like bars and restaurants and shut down sporting events, movie theaters, churches, and offices. The economic fallout of these actions was quick and severe as evidenced by weekly claims for unemployment insurance, which jumped from 282,000 during the week of March 14th to 3.3 million during the week of March 21st, a number not seen since the depths of the Great Depression.

As businesses were forced to shutter and stay at home orders were issued nationwide, the economic outlook for the United States darkened and analysts rushed to determine the impact on all segments of the economy, especially commercial real estate.

How Has Multifamily Been Affected?

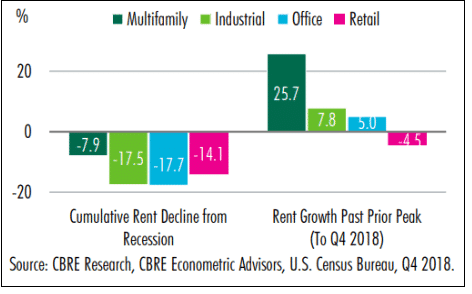

Traditionally, one of the reasons that investors like the multifamily asset class is that housing is a primary need and, no matter their economic circumstance, individuals tend to prioritize their rent payments above all else to ensure they have a safe place to live. As a result, multifamily tends to be the most resilient commercial real estate asset class during an economic contraction. To underscore this point, the following chart from CBRE Research illustrates the cumulative effects on commercial rents during and after the most recent recession in 2008/2009.

To that end, it makes sense to look at the past for clues to how multifamily is performing during the current pandemic. Fortunately, the trend seems to be holding, at least through mid-summer 2020. According to CBRE’s 2020 Multifamily Mid-Year Review, “substantial job losses and very high unemployment led to a significant decline in multifamily demand and rents in the second quarter of 2020. Effective rental rates, including rental concessions, fell an average of 1.00%.”

Going forward, average multifamily rental rates are expected to decline by 8.8% from the Q3 2019 peak to the Q4 2020 trough and vacancy is expected to increase by 3% over the same time period. A gradual recovery through 2021 is expected with demand and rents reaching pre-pandemic levels by early 2022.

Compare this to the retail category, which houses bars and restaurants. The food and beverage industry has been hit the hardest by the COVID 19 pandemic with restaurants accounting for 60% of the 16.8 million jobs lost between March 19 and April 9¹ and the National Restaurant industry estimated $50 billion in lost sales in April 2020 alone. There is significant concern that many temporary closures will turn permanent for those restaurants unable to adapt to a delivery/takeout/outdoor dining model. Permanent closures could cause a substantial increase in retail vacancies and/or high tenant improvement costs to reconfigure dining spaces for a post-pandemic world.

¹ COVID 19 Implications for Reopening Restaurants, CBRE May 2020

Near Term Downside Risks

While multifamily performance has been relatively stable through the early stages of the COVID 19 pandemic, recovery assumptions are wholly dependent upon the idea that a vaccine becomes widely available by the end of 2020, allowing life to return to some level of normalcy. To that end, there are three significant near term risks that could derail multifamily recovery projections:

- Extended Delinquency Moratoriums: On September 4th, 2020 the CDC issued a nationwide ban on rental evictions through the end of 2020. The ban makes it illegal for landlords, multifamily included, to evict tenants for nonpayment of rent. This has a downside impact to multifamily property income and if it is extended for a significant period of time, owner/operators may be unable to continue subsidizing lost income.

- Mortgage Forbearances: Some of the nation’s largest multifamily lenders, including FNMA, have provided loan payment relief for their borrowers in the form of a forbearance. If eviction moratoriums are extended, but forbearance periods are not, there is an elevated risk of multifamily loan defaults, which is a negative for the asset class in general.

- Vaccine Uncertainty: Fundamentally, multifamily demand is tied to jobs and job creation, which provide the income needed to pay the rent. At the time of writing, there is significant hope that a widely distributed COVID 19 vaccine will help the US population achieve a level of herd immunity that would allow life to return to normal. However, if the vaccine timeline is delayed or if it is not widely accepted by a skeptical population, sustained job losses could elevate multifamily delinquencies and decrease demand.

Longer term, there is additional uncertainty about how COVID 19 will permanently impact living preferences. For example, many employers are moving to a work from home or hybrid model which may require owner/operators to adapt existing space to this lifestyle shift.

Conclusions & Summary

The bottom line is that, in light of the current pandemic multifamily performance has been relatively stable to date with early signs of a recovery that is expected to extend into 2021. However, there is still a significant level of uncertainty around a stabilizing job market and debt forbearances.

Individuals considering a multifamily investment should take comfort in the fact that regulatory authorities and lenders have taken proactive steps to provide relief to owner/operators who need it. Given the likelihood of additional government stimulus and an extended period of low interest rates, the outlook for a sustained recovery appears promising.

About First National Realty Partners

First National Realty Partners is one of the country’s leading private equity commercial real estate investment firms. With an intentional focus on finding world-class, multi-tenanted assets well below intrinsic value, we seek to create superior long-term, risk-adjusted returns for our investors while creating strong economic assets for the communities we invest in. To learn more about our investment opportunities, contact us at (800) 605-4966 or ir@fnrpusa.com for more information.